.png?width=1124&height=624&name=MicrosoftTeams-image%20(4).png)

Source: Dalrymple Bay Infrastructure

When you find a company with an attractive business model, it is always worth taking a deeper dive. Whilst the definition of an ideal business model can be quite subjective, I think many would agree that a company which has its cost of revenues covered by the customer is not a bad start. Whilst many companies are spending to directly generate revenue, Dalrymple Bay Infrastructure (ASX: DBI) doesn’t.

DBI has a long-term concession arrangement to operate and maintain the Dalrymple Bay Terminal (DBT) until 2051, with an option to extend this out to 2100. This asset is leased from the Queensland Government, through its wholly owned entity, DBCT Holdings Pty Ltd. Due to this, it is an asset that is regulated by the Queensland Government. It is the world’s largest metallurgical (coking) coal export facility and serves as a global gateway to the global steel making supply chain from the Bowen Basin in Queensland.1

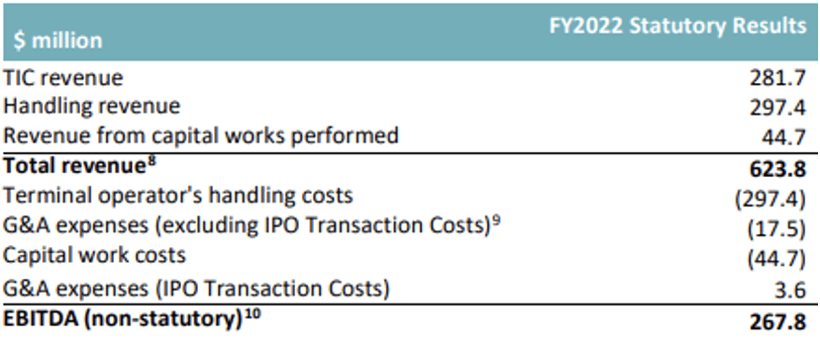

You can see in the table below that DBI has three distinct revenue lines. It quickly becomes clear that the amounts for handling revenue ($297.4 million) and revenue from capital works performed ($44.7 million) are perfectly matched by terminal operator’s handling costs and capital works costs, respectively. This is because in reality, these two lines of revenue aren’t really revenue. It is simply DBI’s costs being reimbursed.

Source: Dalrymple Bay Infrastructure, Appendix 4E and 2022 Full Year Financial Results

Source: Dalrymple Bay Infrastructure, Appendix 4E and 2022 Full Year Financial Results

Essentially, the core revenue line for DBI is the Terminal Infrastructure Charge (TIC) revenue, and its cost of revenue is handling costs, which as mentioned, are paid for by customers. Given this, DBI essentially has a 100% gross margin. To us, that is good business model. DBI is also reimbursed for capital works, which are construction services provided to the Queensland Government. This is because the owner of the asset, the Queensland Government, is responsible for paying for its upgrades, not DBI. This ensures that the facility stays up to date, at no expense to the long-term leaseholder.

As these costs are paid for, the only costs that DBI is paying down to the EBITDA line is general and administration (G&A) expenses. Not many businesses would complain with only G&A as their main costs above the EBITDA line. Due to this, DBI has very high real EBITDA margins. In FY22, this was approximately 95% (using EBITDA / TIC revenue).2

Taking a look beyond its financial statements, we note that the DBT is a high-quality monopoly asset with strategic importance for the region. The DBT provides the lowest cost pathway from the Bowen Basin to international markets on average. The asset currently has an 85 Mtpa (million tonnes per annum) nameplate capacity, which is fully contracted with 100% take-or-pay contracts.3

Take-or-pay contracts mean that users are required to make periodic payments for the processing of contracted volumes, irrespective of whether all of the contracted volume is actually exported through the terminal. The take-or-pay nature of DBI’s long-term contracts further underscores its earnings visibility as these contracts have no throughput risk, meaning revenues are unaffected when the volumes exported from the DBT vary from contracted agreements. This is important as coal exporters may see varying volumes depending on demand, prices, costs and mine-specific issues such as any pauses to mining operations. The type of contract DBI uses is another part of the business model that is attractive.

In addition, the DBT has a well-defined expansion pathway to accommodate further coal volumes in the future. In addition to currently being fully contracted for its existing 85 Mtpa nameplate capacity, the asset also has an Access Queue which it cannot currently service in its current state. Management’s ‘8X Expansion’ plan will add incremental capacity of 14.1 Mtpa over four phases, bringing the asset's total nameplate capacity to 99.1 Mtpa at a total estimated cost of $1.3 billion.4

However, this capacity would be wasted if no one’s shipping it, so we have to consider the outlook for metallurgical coal. Metallurgical coal exports from the Bowen Basin are expected to remain robust in order to satisfy forecast growth in steel production in India and Southeast Asia and we believe the DBT is well positioned to continue being the export terminal of choice for miners in the region.

Crucially, China appears to have started accepting Australian coal again, which is a tailwind for DBI’s earnings.5 China is a huge export market for metallurgical coal. The timing is also good, as China has reopened its economy and the government will be looking to support economic growth. When a government looks to stimulate economic growth, infrastructure expenditure is usually a key component. With steel being a core component of many types of infrastructure, this will drive demand for metallurgical coal.

When looking at DBI, one question that may arise is its long-term exposure to coal, given that there is a global shift away from the long-term use of coal. Although coal is not looked upon favourably over the long-term, it is important to note that over three-quarters of exports from this terminal are metallurgical coal, which is essential in the steelmaking process. This process is called basic oxygen steelmaking, which requires the use of a basic oxygen furnace (BOF), which is powered by metallurgical coal.6 Whilst there are viable alternatives to thermal coal, there is no viable alternative to metallurgical coal that matches the efficiency and cost-effectiveness of BOF steelmaking at the moment.7

While there is much debate about how much and how long thermal coal should be used for, this is a separate issue, and there isn't much evidence that metallurgical coal will be efficiently replaced anytime soon. Due to being grouped in with thermal coal, we believe that the durability of demand for metallurgical coal in the medium to long-term has been underestimated by some. When alternatives to metallurgical coal become viable due to technological advancements, management has already begun exploring future export options for other commodities that will be critical in the future, such as hydrogen and ammonia.8

As mentioned, the DBT is a regulated asset. It is important to point out that as of 1 July 2021, the Queensland Competition Authority (QCA) approved the transition to a ‘lighter handed’ regulatory framework. Under the new regulatory framework, DBI raised prices for TIC for all clients under a new agreement that lasts until the end of June 2031. The price increases were significant, with the new TIC of $3.18 per tonne in FY22 and FY23 representing a 29% increase over what was charged prior to the new regulatory framework. Prices will be raised in line with inflation until the end of the new agreement as well, which is another attribute that we view as particularly attractive.9

The increase in earnings supports an uplift in dividend payments going forward. Its Q2 FY23 distribution will represent a 10% increase in dividends from the same quarter in the previous year. Due to the new pricing agreement, management have revised their target for distribution increases from 1-2% to 3-7% per year.10 DBI already has an appealing forward dividend yield of approximately 7.85%, which is expected to rise due to the new pricing agreement under the new regulatory framework.11

Reference List

1-5. Dalrymple Bay Infrastructure ASX company announcements

6. ScienceDirect, Coking coal – An overview

7. Australian Financial Review, Need for ‘reality check’ on green steel: BlueScope (July 2022)

8-10. Dalrymple Bay Infrastructure ASX company announcements

11. IRESS